Global Scrap Export Restrictions – 2025 and Beyond!

Home / Global Scrap Export Restrictions – 2025 and Beyond!

Admin30th, Apr 2025

Global Scrap Export Restrictions – 2025 and Beyond!

Overview: A Growing Global Trend

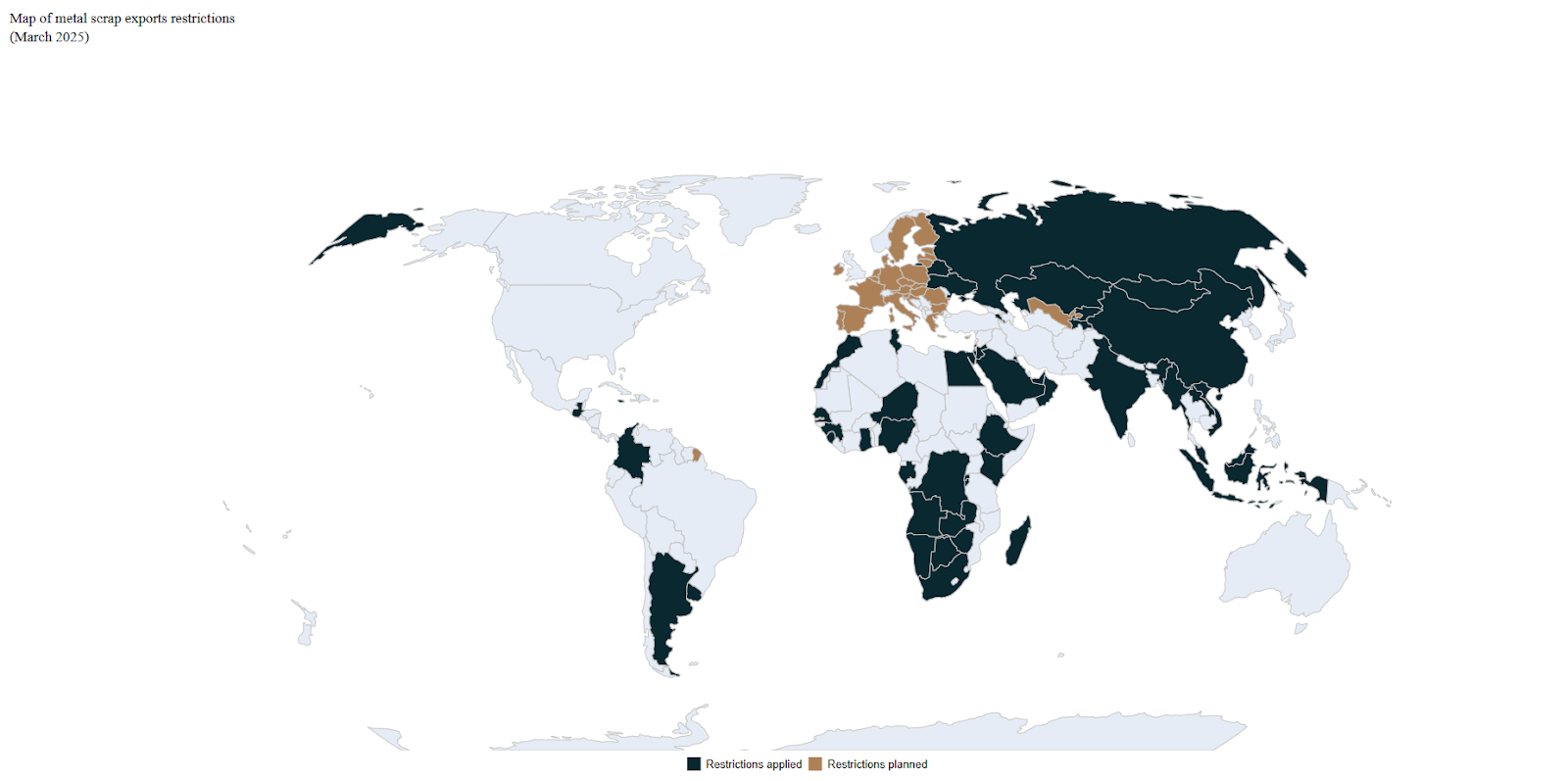

Scrap exports are increasingly being restricted across the globe. As of March 2025:

48 countries have restricted the export of ferrous scrap.

38% of these countries have imposed outright export bans.

With upcoming policies like the EU Waste Shipment Regulation (May 2027) and Uzbekistan’s export duties (July 2025), 76 countries—accounting for 77% of global steel production—will have barriers to ferrous scrap exports.

This shift marks a significant transformation: scrap is losing its status as a free-trade export commodity.

Strategic Resource for Decarbonization Scrap is essential for low-emission steelmaking, prompting countries to retain supplies for domestic use.

Steel Production Policies Over 1.5 billion tons of crude steel is produced annually in countries implementing or planning export restrictions.

Support for Green Steel Industry Affordable domestic scrap prices are seen as critical to making “green steel” cost-competitive.

Circular Economy Models Increasing recycled content in goods is a cornerstone of climate policy and requires secure scrap supplies.

Trade Parity Countries are introducing similar barriers to level the playing field with others who already regulate exports.

Key Future Trends in the Global Scrap Market (GMK Center)

Continued increase in trade restrictions on scrap exports.

Emergence of new restriction types aligned with climate goals.

Scrap will be consumed more domestically than traded.

Growing local demand will lead to higher global scrap prices, while local markets may regulate prices through policies.

The scrap market will experience widening price differences between global and local levels.

EU scrap consumption will rise due to decarbonization and CBAM.

Global scrap trade volumes will decline over time.

Global Steel Scrap Demand Outlook

Global demand for steel scrap is projected to increase by nearly 50% by 2050. The primary drivers:

1. Increased Scrap Usage in Steelmaking

The share of scrap in steel production (metallics) is set to grow from 30% to 45% by 2050 (Mission Possible Partnership, IEA, E3G).

2. Expansion of Electric Arc Furnace (EAF) Capacity

EAFs use scrap as their primary input. The OECD forecasts EAF-based scrap consumption to more than double from 360 million tons in 2019 to 820 million tons by 2050.

Country-Level Scrap Demand Growth

China:

Scrap consumption to increase by 63%, reaching 350 million tons by 2030 (China Association of Metal Scrap Utilization).

India:

Demand projected to double from 34 million tons in 2024 to 70 million tons by 2030 (Kallanish Commodities).

Scrap Supply vs Demand Outlook

Boston Consulting Group estimates:

Demand CAGR (2023–2030): 3.3%

Supply CAGR (2023–2030): 3.0%

Expected Deficit by 2030: 15 million tons

In 2023, only 15% of the 650 million tons of global scrap consumption came from international trade. The rest came from domestic merchant supplies and home scrap.

With limited room for increasing home scrap generation, domestic merchant scrap will become essential.

Global Scrap Trade – Current Trends

Global scrap trade volume remains stable, fluctuating around 99 million tons.

No growth despite the increase in global steel production between 2015–2021.

Trade is highly concentrated:

Top 5 exporters: 47% of total exports.

Top 5 importers: 49% of total imports.

Country Examples:

Türkiye: Largest importer; relies on EU, US, UK, and Russia. Some Turkish steelmakers have sourcing units in North America.

USA: Both a major exporter and importer. Faces shortage in prime scrap and imports from Canada.

Japan: Exports excess prime scrap to South Korea, Southeast Asia, and China.

EU and Scrap Export Restrictions

The EU is the largest scrap exporter, accounting for nearly 20% of global scrap trade. From 2015 to 2021, EU exports of scrap doubled.

Issues:

Scrap “leakage”: High-paying third countries importing EU scrap instead of it being used domestically.

These countries often subsidize recycling, creating unfair competition and overcapacity.

Missed opportunity for supporting European decarbonization goals.

EU Actions:

New Electric Arc Furnace Projects

EU EAF capacity projected to increase by 60%+ compared to 2024 levels.

Additional scrap is required, even with DRI (direct reduced iron) development.

Regulatory Changes

Amended Waste Shipment Regulation (effective May 21, 2027):

Bans scrap exports to non-OECD countries that can’t manage waste sustainably.

Steel and Metals Action Plan (Q3 2025):

May introduce trade measures to ensure internal scrap availability.

Global Impact:

EU restrictions will likely trigger similar measures worldwide, reshaping global scrap flows.

Conclusion: A Shift to Domestic Supply Dominance

As global scrap demand rises and export restrictions increase:

Domestic merchant scrap will become the primary supply source.

Scrap will no longer be a commodity for free trade, but rather a strategic resource.

These changes will underpin the transition to green steel and a more self-reliant, circular economy for many nations.